Getting a job, maintaining a decent credit history, saving up for a deposit, and applying for a home loan has been the most straightforward way of owning a property in Australia. But was it always this systematic?

Below is a quick rundown of the Australian home loan timeline. It puts into perspective the events that define Australian mortgages today, right from the inception.

Home Loan Timeline: The Late 19th Century

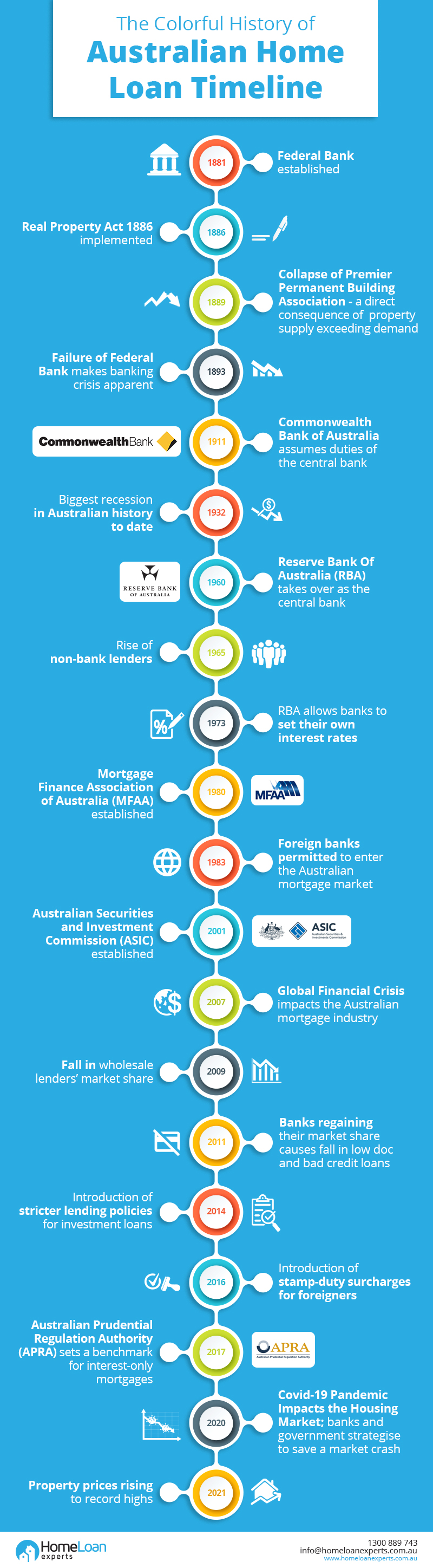

1880s

Real Property Act

The Australian home loan timeline started with the adoption of the Real Property Act 1862, first by Victoria, followed by other states. However, the property rights across Australia we know of today got introduced a little later in 1886 in South Australia. The Real Property Act 1886 aimed to identify and record the ownership details of land or property to reduce the rate of fraudulence occurring at the time. Through this act, people were able to register their entitlement to a property, including mortgages.

Impact Of An Unregulated Banking System

Australian banks operated in a free banking system even after establishing the Federal Bank of Australia earlier in 1881. The federal bank issued the banknotes but did not regulate the banking system like a central bank. It was around this time that there was substantial speculative demand in the property market. And the establishment of a large number of building societies and land banks began. The supply well exceeded the demand for property. A direct result was the collapse of the Premier Permanent Building Association in December 1889, one of Melbourne’s largest building societies. Following the collapse, more small banks and building societies shut down in 1891. Finally, the failure of the Federal Bank in January of 1893 made the banking crisis apparent. By May of the same year, eleven major commercial banks throughout the country had suspended trading.

Home Loan Timeline: 1961-1970

A Proper Central Banking System

The Federal Bank’s Failure made the need for a separate central bank evident to restore public faith in the banking system. Thus, the Commonwealth Bank of Australia (CBA), a commercial bank established on 22 December 1911, got the central bank authority in 1920. It was the first bank to receive a federal government guarantee. The guarantee meant that the government took on the responsibility of securing all deposits in the bank. As the central bank, it took over the responsibility of issuing Australian banknotes from the Department of Treasury.

Heavily-regulated Financial System To Control Recession

In the 1990s, the government revenue saw a severe downturn, with most economic sectors not doing well. As a result, there was a cutback in borrowing as well as government expenditure. The recession became worse when most other nations fell into recession, and foreign investments stopped flowing. The demand for Australian export shrunk, too.

The biggest recession in the history of Australia peaked between 1931 and 1932. Post-recession, as a tactic to avoid another recession, Australian government authorities put in place the following regulatory measures:

- Took control over setting interest rates.

- Put a limit to the number of loans given by one bank.

- Set the minimum amount for banks’ reserve capital.

Needless to say, banks were giving out a lesser number of loans, to stay inside the regulation.

Establishment Of RBA

The CommonWealth Bank (CBA) started facing criticism for operating as a central bank and commercial business at the same time. So, in 1960, the Australian Government established the Reserve Bank of Australia (RBA), which took over as the central bank. Today, its main function is to produce banknotes, regulate the banking system, and announce cash rates.

Lenders Mortgage Insurance

Established in 1965, The Housing Loans Insurance Corporation (HLIC) offered lender insurances. Its insurance policies covered the losses suffered by lenders if a borrower were to default on their mortgage. The insurance encouraged banks to be less strict with the lending criteria because even if the borrower defaulted, they got a backup. This insurance today is known as Lenders Mortgage Insurance (LMI).

Rise Of The Non-banks

Most of the events that unfolded in the 1960s led to a highly regulated banking system. Banks were doing the bare minimum to provide borrowers with better Loan to Value Ratio (LVR) and competitive interest rates. Non-bank lenders started to rise in the market to provide the borrowers with better deals and packages. Banks lost their market share for mortgages from 90% in the 1950s to 70% in 1970. It was evident that, with banks being inefficient in satisfying their needs, they started shifting to non-banks.

Home Loan Timeline: The 2000s

1973

RBA set the banks free from capital requirement so they could set their own interest rates.

1980

Establishment of The Mortgage Finance Association of Australia (MFAA) provided representation and accreditation to all operators in the mortgage industry. Individual mortgage brokers could sign up to MFAA and get their broker license.

1983

Australian government allowed foreign banks to enter the market. There was an increased competition in the mortgage industry.

1989

The removal of separate categorization of savings and trading banks gave an opportunity to extend home loan types from residential to commercial purposes.

Home Loan Timeline: The 1990s

Rise Of Wholesale Lenders

By 1996, wholesale lenders’ market share increased by 4% compared to 1993. They were offering more competitive rates than lender banks and even non-banks. They also introduced competitive home loan products such as:

Establishment Of APRA

The Australian Prudential Regulation Authority (APRA) was established on 1 July 1998. Its principal function is to oversee and report financial institutions’ actions, including banks and the mortgage industry as a whole. Its job was also to establish and enforce prudential standards and practices to ensure a competitive financial system.

Home Loan Timeline: The 2000s

The Early 2000s

In the early 2000s, banks began increasing the discounts offered on their standard interest rates.Various lenders offered a new range of products to meet the needs of those who could not meet standard lending criteria. By 2004, 10% of home loans approved in Australia were low doc loan products.

Lenders also introduced new mortgage features such as redraw facilities, offset accounts and line of credit so borrowers could better manage their mortgages.

Also, In 2001, the government established The Australian Securities and Investment Commission (ASIC). It regulates Australia’s corporate markets and financial services sectors.

The Global Financial Crisis (GFC)

Due to the US housing bubble that peaked in 2004 and the rise of defaults in home loans, the GFC hit Australia around mid-2007. The wholesale lenders were affected the most by GFC because they would bring in the international market’s funding to provide cheap interest rates. Them not providing competitive rates due to the global crisis meant borrowers saw no reason to choose them over banks.

As a result, wholesale lenders’ market share fell from 13% in mid-2007 to about 2% by early 2009. Major banks also bought some wholesale lenders. And thus, the market share for banks rose from 60% to 80% over the two years. With banks regaining their market share of borrowers, there was a tightening of lending policies.

Home Loan Timeline: The 2010s

The banks regaining their market share and wholesalers losing theirs led to a drastic fall in low doc and bad credit loans in 2011. The demand for loans hence decreased, and supply was ever-growing. To avoid a potential market crash, the RBA was cutting the official cash rate continuously. The Australian government began offering various grants and schemes to entice first home buyers to buy a new property. Specialist lenders also entered the space to fill this market gap.

Stricter Lender Policies For Investment Loans

By 2014/15, the RBA began introducing stricter lending policies for investment loans. It then required every lender to make investor lending to no more than 10% per annum of their total loan book. The government began cracking down on foreign investors by increasing the penalties for those who breached foreign investment rules.

Stamp-duty Surcharges For Foreign Buyers

All Australian states introduced stamp-duty surcharges for foreign buyers in 2016.

APRA Sets Benchmark For Interest-only Mortgages

On closely monitoring residential mortgage lending trends for over three years, APRA, in 2017, concluded the presence of a risky mortgage practise. It mandated all Australian Depository Institutions (ADIs) to set their interest-only lending at 30% of their book value. Further, it placed stricter internal limits for interest-only loans provided for the Loan to Value ratio (LVR) above 80%.

Establishment Of The Banking Royal Commission

The big four banks were under scrutiny for alleged misconducts like benchmark interest rate meddling and mortgage fraud. Thus, on 14 December 2017, a Banking Royal Commission was established. Its main function was to check on any frauds in the banking, superannuation, and financial services industry. It submitted its final report to the governor general on 1 February 2019.

Toughening Of Australia’s Lending Standards

Following the establishment of the Banking Royal Commission, limit of interest-only loans, and lenders moving away from high-risk loans, it became harder to get mortgages. In 2018, lenders, to bring their reputation back in line, were setting lending standards stricter than in several years. The growth in home loans was evidently on a decline with 5.87% new loans given out in 2018 versus 6.6% the previous year.

Benchmark For Interest Only Loans Removed

A substantial strengthening of Australian mortgage lending standards led APRA to lift the interest-only benchmark on January 1, 2019. The Australian Depository Institutions (ADIs) were required to provide substantial assurance of improved lending standards to lift the benchmark.

Home Loan Timeline: The 2020s

Covid-19 Pandemic Impacts The Housing Market

The economic crisis brought about by the Covid-19 pandemic started showing its effect in the Australian housing market a little late. Usually, it takes property prices to be hit by the impact of economic fluctuations, the reason being, houses are harder to buy and sell than stocks and bonds. Nevertheless, the economic crisis did catch on to the mortgage market in the first quarters of 2020. As a result, initially, there were mortgage defaults, repayments due, a decrease in home loans, and a fall in property prices. All of this, mainly due to the unemployment rates skyrocketing.

However , the Australian government and the mortgage industry was quick to predict such changes and hence they were able to implement defensive measures soon enough.

From a lenders’ point of view, for the one’s unable to make repayments due to the pandemic, mortgage deferral dates were set. On 31 December 2020, official data on deferrals was submitted by Australian Deposit-Taking Institutions (ADIs). It showed a total of $51 billion worth of loans on temporary repayment deferrals, which was around 1.9 per cent of total loans outstanding. Covid-19 Assistance Schemes To cut down the pandemic’s effects on economically impacted home buyers, the government introduced various schemes.

Of the schemes provides, some of the most sought schemes were:

- HomeBuilder Grant

- Job Keeper

- Extension of FHLDS Scheme

RBA interest rate at a record low of 0.1% In November 2020, RBA cut the official cash rates to a record low of 0.1%. Before this, the lowest RBA had ever gone with its cash rate was 1.5% in 2020. This drastic measure had to be taken because Australia was still under recession. The direct impact on borrowers from the low cash rates was that banks could now provide home loans at the lowest interest rates possible.

Rise In Property Prices (2021)

As the economy slowly started to recover in 2021, the property market became a seller’s market. With the remote working experience and a lack of space, the demand for spacier accommodations created a demand-supply imbalance. The demand outweighing the supply caused an increase in property prices all over Australia.The prices are likely to shoot up throughout 2021, setting new records. Also, the lenders started to bring their guards up regarding high-risk loans.

As they plan on setting higher rates in the coming month, they also started to slow down their lending altogether.

With many changes underway, it would be interesting to witness what turn of events come in the Australian home loan timeline in the days to come.

How Do I Get A Home Loan Today?

If you want to know what you need to do today to qualify for a home loan, please call us on 1300 889 743 or fill in our free assessment form and discover how our award-winning service can help you qualify.