Will Your Gift Letter Format Be Acceptable To The Bank?

If you’re like one of many Australians, you may have asked your parents to gift you the money for your deposit.

With some lenders, a gifted deposit means you don’t need to prove genuine savings and essentially get into the property market with no deposit.

The trick to getting approved is using a gift letter template that the bank will accept as proof that the money from your parents is non-refundable.

Why Might The Bank Need A Gift Letter?

A gift letter is a letter from your parents or a close relative confirming that they are giving you a gift for you to use as a deposit to buy a property.

Lenders need to confirm the source of a borrower’s deposit to make sure they are not borrowing the deposit off credit cards or a personal loan.

Some Australian lenders won’t lend to people who have received their deposit as a gift.

Please read our page about home loans with a gifted deposit for more information about the loan options available to you.

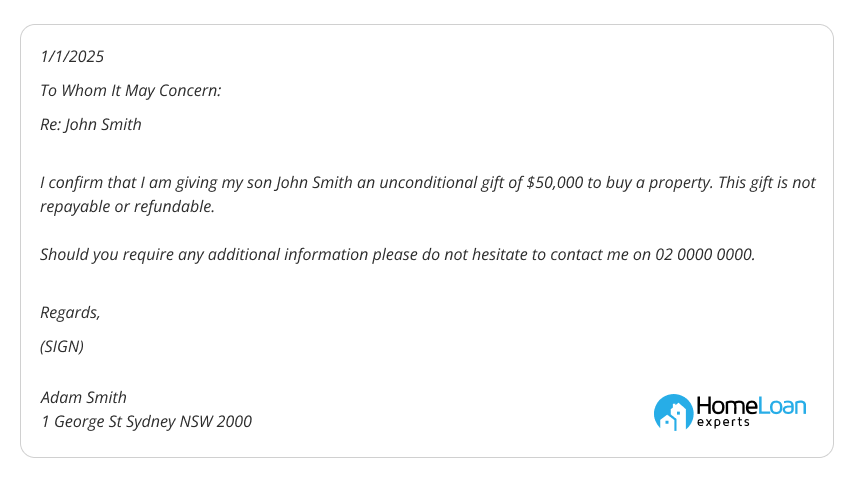

Gift Letter Template 1 – Standard

This is the gift letter template for a mortgage that’s accepted by most lenders.

If your lender has specifically asked for a statutory declaration then please use the 2nd template.

If a Home Loan Experts mortgage broker is arranging your home loan, please email your signed letter through to them.

Which lenders will accept a gifted deposit? Call us on 1300 889 743 or enquire online to find out.

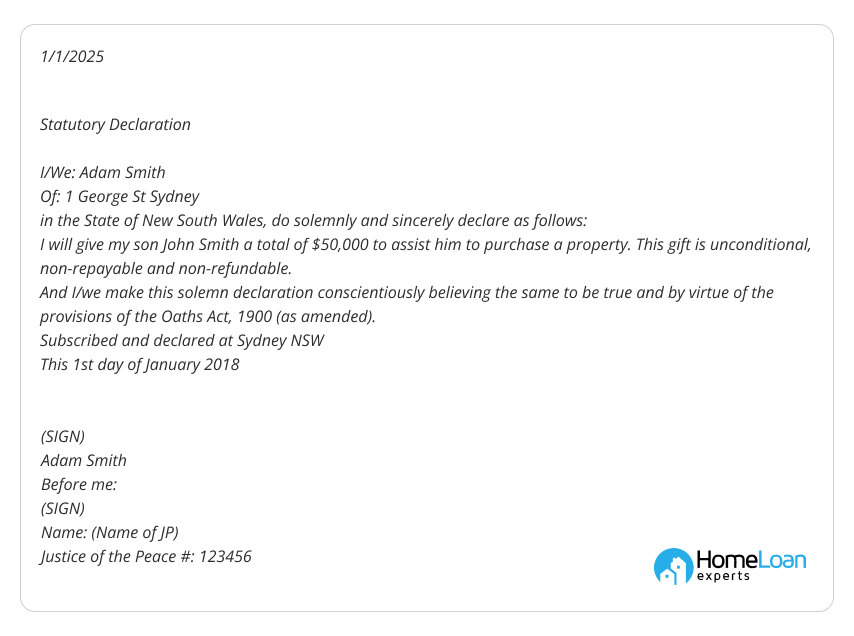

Gift Letter Template 2 – Statutory Declaration

Use this mortgage gift letter template if your lender has specifically asked for a statutory declaration.

Please note that some lenders such as Suncorp have their own statutory declaration template.

If you’re unsure what template to use, please call us on 1300 889 743 to discuss.

If a Home Loan Experts mortgage broker is arranging your home loan, please email your signed letter through to them.

Which lenders will accept a gifted deposit? Call us on 1300 889 743 or complete our free assessment form.

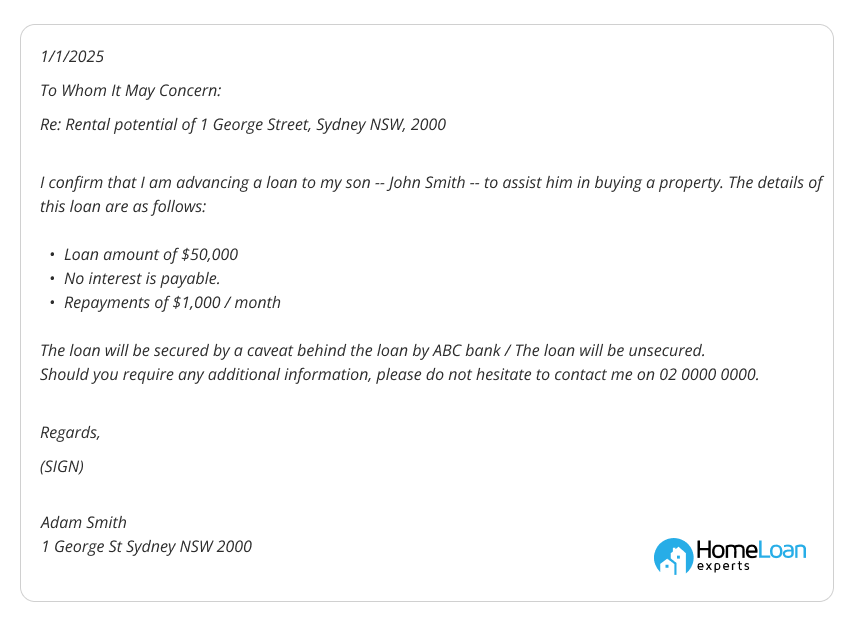

Gift Letter Template 3 – Family loan

In the event that the gift is repayable, this is assessed as a borrowed deposit by the banks.

If you get a loan from a family member to help you buy a property, only a select few banks will consider your application.

Please contact us if you’re having trouble finding a lender.

If a Home Loan Experts mortgage broker is arranging your home loan, please email your signed letter through to them.

Which lenders will accept a gifted deposit? Call us on 1300 889 743 or complete our free assessment form.

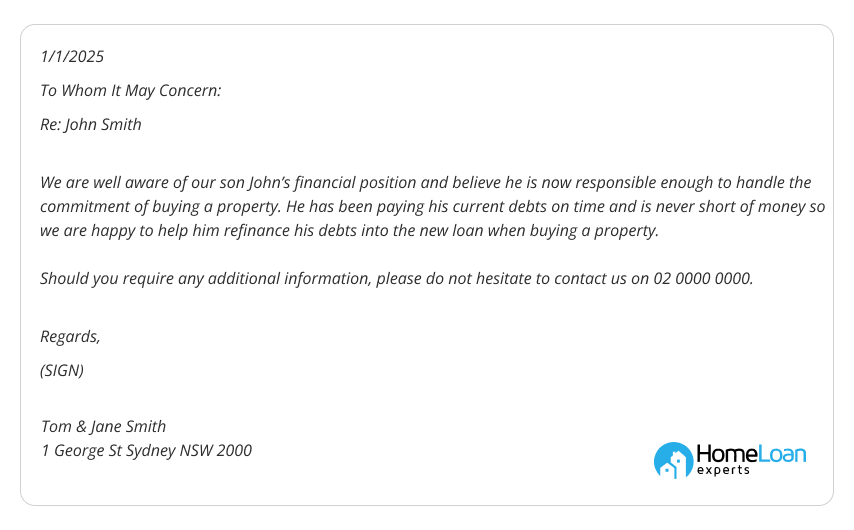

Gift Letter Template 4 – Guarantor support

If your parents have decided to use a property they own as additional security for your loan then we may require a letter from them confirming that they are fully aware of what they’re doing.

This is particularly important if you’re consolidating debts while buying a property.

The letter must be signed by all guarantors.

Simplify the mortgage maze with the 360° Home Loan Assessor

Get results on:

- Your maximum borrowing power

- The hidden costs of buying a home

- Interest-rate options based on your situation

What Catches People Out?

Did you know that some banks have a policy which allows them to accept a gift as a deposit, yet their credit scoring system assesses these applications in a very harsh way.

As a result, many people get declined.

Secondly, some people are actually borrowing their deposit from their parents and intend to repay it later.

This is a loan, not a gift, and only a few lenders specialise in this kind of lending.

The key is to apply with a lender that sees people with a gift as a low risk borrower.

Bank Requirements For Gift Letters

Australian lenders have strict requirements for letters confirming the source of a deposit and will often ask for a letter to be amended if it doesn’t meet their requirements.

Your gift letter should be:

- Dated.

- Signed.

- Contain the name of the person who signed the letter.

- Contain the name of the person receiving the gift.

- Confirm the gift amount.

- Confirm that the gift is “unconditional, non repayable and non refundable”.

Most lenders will accept a faxed copy but some will require your mortgage broker to hold the original on file.

Which Bank Can Approve Your Loan?

Our mortgage broker brokers are experts in no deposit home loans and we know which lenders can accept a gifted deposit in lieu of genuine savings.

Please call us on 1300 889 743 or complete our free assessment form to speak to one of our experienced staff.