What Is Bricklet-AMP Low Deposit Shared Equity?

Bricklet, a platform for shared-equity home loans, has partnered with AMP to offer buyers home loans if they haven’t saved up a large deposit but can service a loan. Investors will have shared equity with buyers. They will provide 20-40% of the cost of the property. Buyers can offer a deposit of as low as $10,000-$20,000; some properties will also be available with no deposit. The buyer then borrows the rest through a mortgage and pays rent to the investors on the portion they own.

While buyers will be registered as co-owners with investors, they will be 100% owners on the land title, and investors will be written as a caveat on the title.

Buyers retain majority ownership of the property and control how it is used. They can renovate the property while living there.

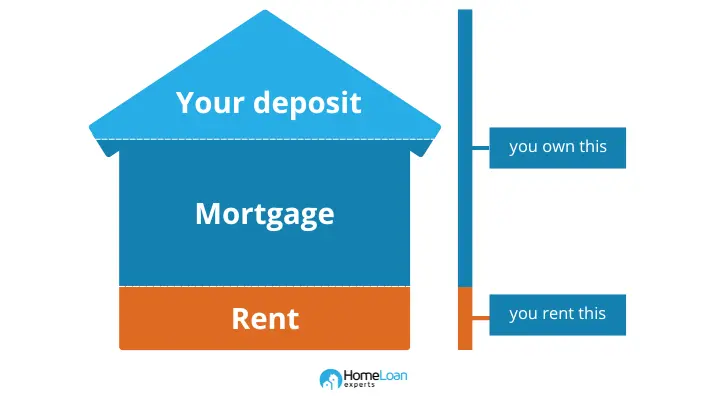

The above figure depicts how equity is broken down. The deposit is the share initially put in by the homebuyer, the mortgage area represents the amount loaned by the bank and the rent area is the amount the investor pays upfront.

Who Is This For?

Bricklet CEO Darren Younger said, “The shared equity platform was created on the basis that many people don’t qualify for government schemes. They either have too much, have already owned before, don’t meet the price cap, or miss out because spots are limited.” Bricklet will accept all buyers who pass AMP’s lending and serviceability criteria for a home loan.

Pre-Qualification Requirements for AMP

- You have to be over 18 years old.

- You have to be an Australian or a New Zealand citizen or a permanent resident.

- Employed full-time, part-time, as a contractor or casual, self-employed.

- You must be looking to borrow above $100,000.

- You seek a home loan to purchase or refinance a residential property.

Note: The arrangement is subject to the approval of the loan portion in accordance with AMP’s lending policies, which is subject to lender’s assessment.

How Does This Low Deposit Shared Equity Model Work?

Three parties will be involved in this: AMP, an investor or investors through Bricklet’s platform, and the borrower. The borrower and the investor/s will be sharing equity in the property.

In addition to the mortgage payment to AMP, the homebuyer will pay the investor an occupancy fee in the form of monthly rent, at 6% of the value of the shared equity.

Here’s an example of the breakdown with figures, based on a property with a value of $800,000:

From the figure above, assuming that the homebuyer is looking at an $800,000 house and has saved $20,000 to put down as a deposit, and AMP gives approval:

- Bricklet investors put in $200,000 (25% of the property value) so, the homebuyer will have to borrow $580,000 from AMP.

- The Loan-to-Value Ratio will be 72.5%, which means the homeowner doesn’t have to pay Lenders Mortgage Insurance (LMI).

- The homeowner will own 75% of the property, and investors will own 25% of the property.

- The homeowner will have to pay a monthly rent of $1000 (6%) to investors ($200,000 * 0.06)/12 = $1000

- Mortgage interest rates will be at AMP’s discretion.

What Do I Have To Contribute?

Buyers will have to make an upfront payment of the stamp duty, Bricklet set-up fee and a deposit.

What Are The Regular Payments I Have To Make?

- Monthly occupancy fee starting from 6% of shared equity. This is a monthly payment to investors and does not reduce the balance of equity owed to the investor.

- Monthly mortgage repayments to the bank.

- Monthly Bricklet administration charge.

When Do I Have To Pay The Investor?

The equity ownership time limit is 10 years. At the end of the contract, a buyer can purchase the equity from the investor, sell off the property and pay the investor their share or refinance the shared equity with a bank and buy the equity from the investor.

Can I Use This With A Government Grant?

You can use this with any government grants or programs for which you are eligible. For example, you can use the First Home Owner Grant as your deposit, or if you are in NSW and choose the NSW property tax option, instead of stamp duty, you will have to pay only Bricklet’s fees and a deposit upfront, you’ll pay the property tax annually. The annual property tax repayments are also factored in as an ongoing commitment for the serviceability assessment.

Can I Sell The House Anytime?

Yes, you can. From the sale of the house, the mortgage has to be paid off, investors get paid their percentage of the equity at the appraisal value, and the homeowner receives the remaining amount.

Pros and Cons Of Using The Shared Equity Scheme

The Pros

- You don’t have to pay LMI, as investors can offer you the 20% minimum deposit.

- You don’t have to wait to buy a house if you have yet to save up a deposit and are earning well enough to service a home loan.

- You will have more borrowing capacity to look at more expensive homes.

- The bank will view you as less risky, so you are more likely to get home loan approval, lower interest rates, and be offered good loan products.

The Cons

- There is a high Bricklet set-up fee.

- You don’t fully own the property.

- You have to make a monthly rent payment to the investor.

- You have to pay back the loan within 10 years. This is less than the 30-year repayment period typically available from banks.

- You’ll have to pay the equity earned on the property to the investor. To explain this, suppose the purchase price of the property was $800,000 and investors provided 25% ($200,000) via Bricklet’s platform, and after 10 years an external evaluation was done and the home was valued at $1 million. The homeowners will have to pay $250,000 (25% of $1 million) back to investors, via Bricklet, to fully own the home.

Interested In The Shared Equity Model?

You can check out our shared equity scheme page to find out about other schemes. You can reach us at 1300 889 743 if you have any questions or fill out our free online assessment form and we’ll get back to you as soon as we can.