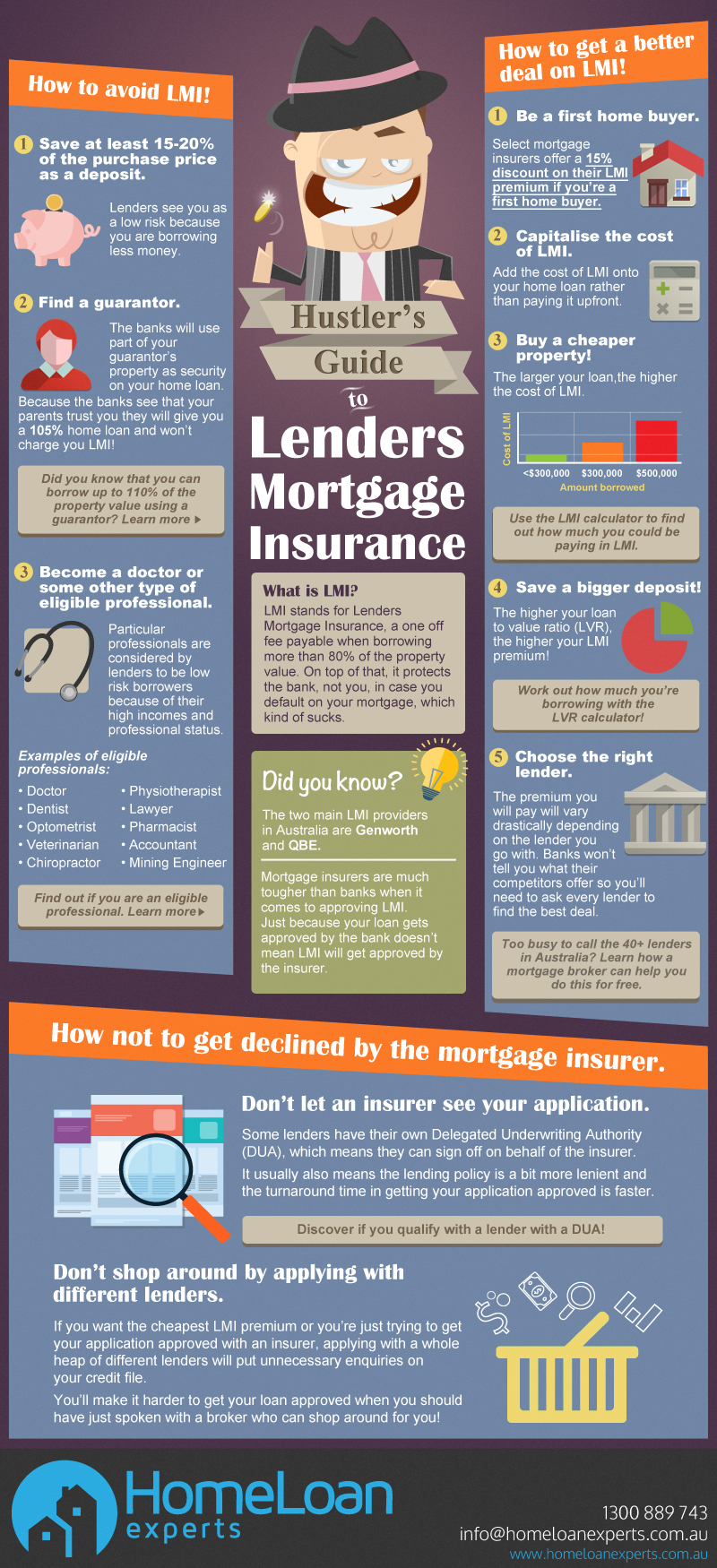

LMI is a one off fee payable when borrowing more than 80% of the property value.

On top of that, it only protects the bank, not you, if you default on your mortgage. It can also be majorly expensive, which kind of sucks!

To put the cost into perspective, if you borrowed $510,000 for a property worth $550,000, your LVR would be over 90% and you could be paying over $23,000 upfront just to get your loan settled.

Worst still is that some lenders will decline your loan just because you’re borrowing over 90% of the property value.

Thankfully, there are ways to get approved and reduce or even avoid mortgage insurance altogether with a little creativity and some help from an experienced mortgage broker.

How to avoid LMI

Want to know how to steer clear of mortgage insurance? Here are a few golden tips:

Save at least 20% of the purchase price as a deposit

By having a 20% deposit, banks see you as a lower risk because you’re only borrowing 80% of the property value.

Ask your parents to go guarantor on your home loan

By having a guarantor provide their house as additional security on your home loan, you will not have to pay any LMI even if you are borrowing 100% of the property value.

How? Because you’ll essentially be borrowing less than 80% of the total value of both properties, meaning no LMI.

You can also cover the other costs of a mortgage including conveyancing fees, stamp duty and other legal costs.

Discover if you qualify by visiting our guarantor home loan page or by contacting our mortgage brokers on 1300 889 743.

Become a doctor!

Okay, we’re pulling your leg a little with this one but it’s true! Certain professionals such as doctors are considered by lenders to be low risk borrowers because of their high incomes and professional status.

Because of this, some lenders are willing to offer discounted home loans including reduced interest rates and waived LMI.

These professionals include:

- Doctors

- Dentists

- Optometrists

- Veterinarians

- Chiropractors

- Physiotherapists

- Pharmacists

- Lawyers

- Accountants

- Mining engineers

Are you a professional? Call us directly on 1300 889 743 and find out what other home loan discounts you may be eligible for!

Don’t qualify for no LMI? Reduce it instead!

If you’re not quite eligible for waived LMI, you may still be able to cushion the premium blow.

Are you a first home buyer?

Did you know that select mortgage insurance companies offer a 15% discount on their LMI premium if you’re a first home buyer?

Available only:

- Through the lenders that deal with these specific LMI providers and have negotiated this discount on behalf of their customers.

- If your home loan is less than $600,000 and your deposit is not from a borrowed source.

Capitalise the cost of LMI

Although you’ll still have to pay the premium, most lenders now allow you to add the cost of LMI onto the principal of the loan rather than you having to put up anything upfront.

Buy a cheaper property!

The larger your loan, the higher the percentage of the loan amount the mortgage insurer will charge you:

- Loans less than $300,000: Very cheap LMI

- Loans between $300,000 and $500,000: Moderate LMI

- Loans greater than $500,000: Very expensive LMI

Even if you’re borrowing $300,001 you could reduce your mortgage by just $1 and immediately save as much as $800!

Save a bigger deposit!

The higher your LVR, the higher your LMI premium.

For example, if you’re borrowing $900,000 secured on a $1,000,000 property then your LVR is 90% and your loan will carry with it a big LMI price tag.

Choose the right lender

The premium you are liable to pay will vary drastically depending on the lender you go with. That’s because different lenders are backed by different mortgage insurers and both the lender and the insurer will assess the risk of a home loan application in different ways.

Lenders do not publish their LMI rates to the general public and do not disclose which LMI company insures their loans.

Use our LMI calculator to discover how much you could save on your insurance just by choosing the right lender.

Talk to a broker

One of the main jobs of a broker is to find out what you want to achieve with the home loan. Do you want to get a cheap mortgage or are you just looking to actually get approved?

If you’re looking to get a good deal, our brokers will look at every single cost associated with the loan including the interest rate, monthly repayments, loan set-up costs andthe cost of LMI.

By doing so they can tell which mortgage insurer will approve your loan, save you the most money and still suit your needs.

Call us on 1300 889 743 today or fill in our free assessment form.

How not to get declined by the mortgage insurer

Don’t let an insurer see your application

Mortgage insurers are much tougher than banks when it comes to assessing your income, employment and your credit file, as well as things like the type of property you’re planning to purchase and its location. Just because your application will get approved with the bank doesn’t mean it will pass the insurer’s policy.

Did you know that not all lenders send your application off to a mortgage insurer to be assessed?

Some of them have their own DUA, which means that the bank can sign off on behalf of the insurer. Generally speaking, it also means that the lending policy is a bit more lenient and the turnaround time in getting your application approved is faster.

There are only a few banks that have DUA. In fact, out of the over 40 lenders on our panel, there are only 10 that have this authority.

Will you pay more?

Actually, at least one of our lenders with DUA has one of the best interest rates on the market and the LMI premium is low compared to some other lenders.

We do have control over whether it goes to an insurer or not by carefully assessing your situation and matching you with a lender that can approve your application without going to an insurer.

Don’t shop around by applying with different lenders

If you’re looking to find the cheapest LMI premium or just trying to get your application approved with an insurer, applying with a whole heap of different lenders will put unnecessary enquiries on your credit file.

Keep in mind that there are only two main mortgage insurers in Australia – Genworth and QBE – so if you’re getting declined for those applications, chances are they are being recorded by the same insurer.

If you can only get yourself approved with that one insurer, you’ve shot yourself in the foot and eliminated your chance with a number of lenders right off the bat.

Apart from the increased chance of having your home loan application declined, shopping around for LMI takes up a lot of time and it’s hard to know if you’re getting a good deal or not.

Home Loan Experts senior mortgage brokers say it’s their job is to present your case in a way so that you’ll win over the mortgage insurer.

“I see myself as a lawyer, so if someone has been declined by an insurer, to me that’s like they’ve lost a court case,” he said.

“Now they’re coming to me, an expert, and they’re trying to get an appeal and, like a lawyer, not every broker has the expertise to do that, but we do.”

We’re LMI experts, so call us on 1300 889 743 or complete our free assessment form.

One of our mortgage brokers will tell you whether you’re in a position to have the cost of LMI reduced or waived altogether!